- Home

- Shareholder Engagement of Corporate Japan [Second Edition]

Part 3 Shareholder Activism and Corporate Control

Chapter 4 Establishing a Market for Corporate Control

Tatsuya Imade

1. What is the market for corporate control?

There is a term “market for corporate control,” which is rarely used in everyday conversation. Where is this market with such a scary name? It is the stock market that you are all familiar with.

In the previous chapters, we have gained a better understanding of shareholder activism and corporate control. Therefore, it should now be clear that purchasing additional shares on the stock market increases the rights to control a company.

Moreover, control can be pursued swiftly through an acquisition proposal that includes a premium over the current market price. Normally, buying shares in the market drives up the stock price, creating a natural premium. In contrast, an acquisition proposal requires the acquirer to secure a majority of shares, which means adding a specific “control premium” to the offer. If multiple acquirers exist, this leads to a bidding war where each increases the premium. In short, a well-functioning market for corporate control enables shareholders to sell their shares at a higher price and make them happy. However, from the acquirer's perspective, there is a risk that a chaotic bidding war will result in a loss of investment, so they will use corporate valuation methods such as the discounted cash flow (DCF) method to find an appropriate upper limit price.

As of the time of writing this chapter, in August 2024, Canadian convenience store operator Alimentation Couche-Tard made an acquisition proposal for Seven & i Holdings – whose core business is convenience stores – for 5.6 trillion yen. After the stock price surged, the Ministry of Finance designated Seven & i as a core industry subject to strict foreign exchange regulations for national security reasons in September. In October, the acquisition offer price was raised to approximately 7 trillion yen, and news emerged of a management buyout (MBO) proposal from a company linked to the founding family (holding 8%) and the current vice president, also a family member (Note 1).

Market observers estimate the MBO at roughly 9 trillion yen. The future developments and Japan's desire to establish and operate a market for corporate control will be tested here. The outcome – potentially Japan’s largest acquisition at 7 to 9 trillion yen – will test Japan’s resolve to establish and operate a market for corporate control. It is also worth recalling the activism by Value Act Capital of the United States in 2022 – 2023 preceding these developments.

2. Various types of corporate acquisition dramas

For younger readers, it is worth noting that Japan experienced a period of intense domestic corporate power struggles from the 1970s through the 1980s bubble economy, including stock buyouts and corporate takeovers. Looking up cases such as Sanko Steamship, Japan Line, and Janome Sewing Machine will provide insight into the circumstances of that era. For those of us who are currently active in the workforce, the series of incidents involving the Livedoor Company and M&A Consulting Company Fund (commonly known as the “Murakami Fund”) in the early 2000s (Note 2) are likely to remain vivid in our memories.

The leveraged buyout (LBO) boom in the United States in the 1980s is another memorable example of the fierce market for corporate control. A symbolic case - RJR Nabisco for 25 billion acquisition – capped the fourth U.S. M&A wave and inspired Barbarians at the Gate: The Fall of RJR Nabisco. The main protagonists were the CEO, who seemed to run the company honestly according to his own desires, and the members of KKR, the LBO fund that won the acquisition battle. At the time, issuing junk bonds backed by the assets of the acquired company made it easier for LBO funds to raise massive amounts of capital. This led to a series of cases where large companies were acquired, dismantled, and employees lost their jobs, sparking social concern. The image of “LBO funds” deteriorated, leading to the adoption of the broader term “private equity (PE) funds” (referring to investments in non-publicly traded shares) as their official designation. In Japan today, MBOs and other forms of privatization (Note 3) have become central features of the landscape.

3. Ecosystem of the market for corporate control

The reforms that Japan has been promoting since Abenomics require the establishment of a market for corporate control. Financing is absolutely essential to the market for corporate control, and the ecosystem comprising banks (indirect finance) and investment banks and securities markets (direct finance) must function properly. Beyond shareholders and creditors, corporate management depends on employees and business partners, so post-acquisition plans are vital. The ecosystem often includes management strategy advisors to support plan formulation, law firms to address legal aspects, media advisors to effectively shape public opinion, and specialists for stock-related operations (e.g., tender offer procedures and shareholder meeting procedures).

Fund activists and institutional investors have become pivotal players in Japan’s ecosystem. A notable development is the rise of “white paper” proposals – management strategy that appear partly outsourced. As mentioned in the previous chapter, it seems that fund activists increasingly assemble cross-functional teams from the ecosystem to produce such proposals.

Activists use ecosystem insights to target attractive companies that lack management approaches centered on capital costs and stock performance – often reflected in depressed share price. They begin investing in such companies, publicly disclose strategic improvement proposals that appeal to general institutional investors holding significant voting rights, and gather public support through traditional and social media. When shareholder voting is poised to reshape the board, a joint MBO proposal from a PE fund may appeal to executives who wish to retain leadership positions and focus on business operations based on the company's history and strategy.

It is important to note that nearly all MBOs are effectively LBOs and PE funds that acquire a majority or all of the shares must ultimately provide absolute returns significantly exceeding the capital costs to the beneficiaries of the fund. Generating returns involves selling to third parties (including business divisions) and relisting. Ultimately, these methods do not deviate from the logic of capital and the market. On the other hand, since this ecosystem of the market for corporate control also includes acquisitions by other operating companies, a market game perspective suggests that undervalued stocks tend to converge toward the upper bound of fair value, regardless of who comes first.

What are the obstacles to the establishment and function of a market for corporate control, which is necessary for Japan's reforms? The most obvious examples are “takeover defenses” and “stable shareholders,” in which companies agree not to sell their shares and to continue supporting the company’s proposals. These two obstacles are gradually being removed through campaigns by institutional investors to abolish “pre-announced takeover defenses” and reduce the number of “cross-shareholdings.” It is clear that the policies that began with the Japan Revitalization Strategy are aimed at corporate restructuring and business reorganization and that the revitalization of the market for corporate control will be the driving force behind the success of these policies. If this strategy succeeds, it is probably correct to assume that the international competitiveness of Japanese companies will be strengthened. However, there is no guarantee that the main body of a company whose competitiveness is strengthened will remain Japanese-owned.

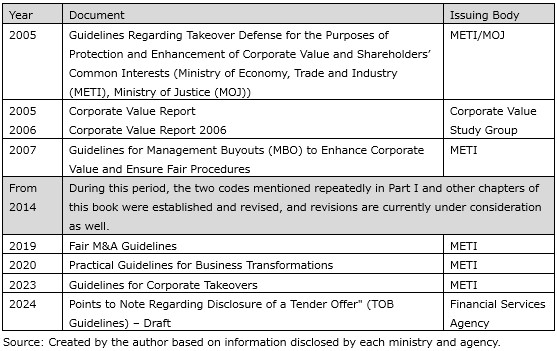

Figure 3-4-1: Domestic policy guidelines and other relevant documents pertaining to the corporate control market

4. Guidelines for Corporate Takeovers

In August 2023, Ministry of Economy, Trade and Industry (METI) published Guidelines for Corporate Takeovers: Enhancing Corporate Value and Securing Shareholders’ Interests (Note 4) with the "objective of encouraging acquisitions that are favorable for the economy and society to occur in a healthily functioning fair M&A market.” The guidelines also updated similar content in previously established guidelines related to corporate acquisitions. The guidelines provide an easy-to-understand overview of the market for corporate control and policy directions outlined in this chapter. We recommend that readers of this book read them carefully.

The guidelines draw particular attention to “acquisitions without consent” (takeover bids that have not been agreed to in advance by the management or board of directors of the target company, formerly known as “hostile takeover bids”). If such bid is a “sincere offer,” the board of directors of the target company should give “sincere consideration.”

In summary, a “sincere offer” is defined as “an acquisition proposal that is specific, rationale, and feasible, corresponding to the English term ‘bona fide offer’” (Note 5). Sincere consideration means "a reasonable effort should be made to ensure that the acquisition will be based on terms that will secure the interest which shareholders should enjoy, in addition to determining whether the acquisition is appropriate from the perspective of enhancing the company’s corporate value.“ When the board of directors gives ”sincere consideration,“ they should ”obtain additional information from the acquiring party about the acquisition proposal, and should consider the appropriateness of the acquisition from the perspective of whether the acquisition will contribute to enhancing corporate value, with a focus on the post-acquisition management strategy, the appropriateness of the purchase price and other transaction terms, the acquiring party’s financial resources, track record and management capabilities, and the feasibility of successful completion of the acquisition." It also suggests "if the company’s stock price is significantly below the proposed price, that may provide an opportunity for the board of directors (especially outside directors) and the management team to recognize the issue of why such a discrepancy occurs, and to consider and analyze the situation." In addition, it states that the aim is to facilitate “desirable acquisitions in Japan,” so if this progresses as intended, it is likely to be positive for the Japanese economy.

Institutional investors and related parties have broadly welcomed the guidelines’ definition of “corporate value” as “the sum of the discounted present value of cash flows that a company will generate in the future,” as this term had previously been subject to ambiguous interpretation and had caused mismatches. This is because engaging with companies based on the DCF method, which is widely accepted and versatile in analysts' corporate analysis and M&A transaction valuations, would enable investors to share a common understanding within the familiar framework of finance theory.

The fact that the guidelines specifically mention “’Corporate value’ is a quantitative concept. The target company management should not make the concept of corporate value unclear by emphasizing qualitative value, which is difficult to measure, nor should the ‘corporate value’ concept be used as a tool for management to defend themselves (including management referring to retention of employees as an excuse to defend themselves)” suggests that there have been significant mismatches in the engagement to date. However, the guidelines reserve interpretation regarding the “intrinsic value” of companies and businesses as follows, leaving room for potential differences in methods for quantitatively evaluating corporate value and intrinsic value:

There can be various views on what the “intrinsic value” is. For example, sometimes the term “intrinsic value” is used as a term substantively equivalent to the term “corporate value” defined in the guidelines (i.e., sum of the present values of discounted future cash flows generated by a company). In the guidelines, the per se value of a company that can be realized through effective exploitation of the company’s current operational resources through efficient corporate management is described as the “intrinsic value.” Some advocates point out that “intrinsic value” in this sense can be objectively evaluated to a certain extent based on analysis with comparable companies (Ministry of Economy, Trade and Industry 10).

In my opinion, as long as we continue to use the Japanese term “corporate value” in its broad sense (Note 6) with its strong connotations of “the spirit of words” (Note 7), there will always be room for non-financial and difficult-to-quantify elements such as culture and spirit to creep in, and there is a possibility that the engagement only on general finance theory will continue to diverge from public sentiment. However, this is not necessarily a bad thing. If the content of the engagement deepens in line with the guidelines’ premises, that would be a positive development.

The guidelines also address activist tactics frequently aimed at achieving a certain degree of management control by replacing many directors – without explicitly stating their intent to acquire management control – as follows:

In relation hereto, there is another issue regarding transparency in cases of corporate control acquisition, where a shareholder proposing an election or dismissal of directors acquires a significant amount of shares in concert with other shareholders, without disclosing its intention to acquire corporate control, and subsequently requests a convocation of the shareholders’ meeting to resolve its proposal to replace the directors with those whom it can influence. Such a situation involves the possibility that a specific party may acquire corporate control without the shareholders deciding on the pros and cons of the acquisition (as a result of the dispersion of shareholdings among multiple parties, there also may be a risk of violating or circumventing large-shareholding reporting regulations). In addition, when a request to convene a shareholders’ meeting is made, the issue of insufficient information is likely to arise because relevant information is not disclosed in the reference documents for the shareholders’ meeting, in contrast to a tender offer. For these reasons, when making a request to convene a shareholders meeting to replace a number of directors for the purpose of acquiring corporate control, it is advisable for the acquirer requesting for the meeting to furnish shareholders with a summary of the purpose of the request, the person requesting the meeting (and the persons, if any, who have agreed with the person requesting for the meeting on the acquisition or disposal of shares, or the exercise of rights as shareholders), the basic management strategy after the proposal is approved, and other appropriate information at least to the same extent as that contained in the tender offer registration statement (Ministry of Economy, Trade and Industry 31).

5. Conclusion

Learning about the “non-consensual” takeover bid for Seven & i Holdings by a foreign company, Japanese people are a little concerned probably because they are aware that the company’s business is deeply rooted in their daily lives as part of the national infrastructure. On the other hand, the company’s global growth as the largest convenience store chain in the US is largely due to its overseas expansion, including the acquisition of Speedway in the US (Note 8). The market for corporate control is changing rapidly. At the time of writing, the acquisition of US Steel by Nippon Steel (a consented acquisition proposal) remains unresolved amid indications that President-elect Trump seems to have plans to block it. Additionally, the merger deal between Nissan Motor, which faces poor performance and stock price conditions, and Honda Motor, is making headlines, with Hon Hai Precision Industry’s actions potentially relevant. Effissimo Capital Management (ECM), a major activist, has surfaced among Nissan Motor’s shareholders (Note 9). ECM also holds a 30% stake in Nissan Shatai and was also the largest shareholder of Toshiba, which has been delisted from the stock exchange. In the process of Japan establishing a market for corporate control, fund activism has been given a great opportunity to generate profits and to create wealth for fund investors.

General investors welcome the momentum of rising stock prices due to activist shareholdings, and policymakers who want to realize corporate restructuring utilize the voices of fund activism. This dynamic is likely to continue for some time.

(Note 1) Seven & i Holdings Co., Ltd. Notice Regarding Media Reports. 13 Nov. 2024,

https://www.7andi.com/library/dbps_data/_material_/localhost/en/release_pdf/2024_1113_ir01en.pdf.

(Note 2) Under the leadership of Takafumi Horie, Livedoor achieved rapid growth through numerous corporate acquisitions as a strategic buyer. Meanwhile, M&A Consulting, founded by former Ministry of International Trade and Industry bureaucrat Yoshiaki Murakami, also quickly acquired various shares and engaged in shareholder activism, leading to several cases involving disputes over control of large companies. Subsequently, Horie was convicted of making false statements in securities reports and Murakami was convicted of insider trading related to Nippon Broadcasting System shares – both of which are violations of the former Securities and Exchange Act.

(Note 3) A management-led buyout of the company, resulting in the delisting of its shares.

(Note 4) Ministry of Economy, Trade and Industry. Guidelines for Corporate Takeovers. 31 Aug. 2023,

https://www.meti.go.jp/press/2023/08/20230831003/20230831003-b.pdf.

(Note 5) “Bona fide,” the Latin-origin term, means “sincere,” but it also means “in good faith,” and “bona fide third party” corresponds to “third party acting in good faith.” From this perspective, it can be said that it differs slightly from the definition of “good faith” in Japanese civil law.

(Note 6) For example, if “corporate value” is translated as “Enterprise Value (EV)” in M&A terminology, the meaning will be different. The expression “corporate value, and the common interest of shareholders” used in various guidelines and reports implies that corporate value must ultimately be attributed to shareholder value.

(Note 7) See Introductory Statement, Note 6.

(Note 8) In 2021, Seven & i acquired a convenience store business with gas stations from a major US oil refiner for 2.3 trillion yen.

(Note 9) As Imade discusses in his chapter in Shareholder Engagement of Corporate Japan, ECM is examined in detail (215–17).

Column 6. Demon Slayer and the market for corporate control

“Don't give others the right to decide life and death!” This is the phrase spoken by Giyu Tomioka to his junior, Tanjiro Kamado, the main character of the hugely popular manga and anime series Demon Slayer. This resonates in the market for corporate control – where the rights to decide life and death of companies are bought and sold, and it is the fate of listed companies to participate in this market. It is crucial to navigate this market successfully, avoiding being killed or deprived of control, and instead striving to be kept alive and granted control. Engagement with shareholders, investors, and the market is essential for this purpose. A common reaction when faced with shareholder proposals from activists is to view the shareholders' meeting as a final battle, with the sole goal of winning that battle, and to believe that the battle will be over and peace will reign once the shareholder proposal is defeated. Activists are not the demons in Demon Slayer, but the strongest demons do not disappear even if their heads are cut off; they resurrect and new demons continue to appear. In other words, engagement with activists is a continuous game centered on the power to grant or withhold life and death over the company.Column 7. Soccer team and listed company

The first step in corporate control is gaining control of the board of directors and replacing a CEO. Imagine that you are an employee of a listed company and that your company sponsors a soccer team that keeps losing. The likely outcome: the coach is dismissed and replaced. In many cases, the team's enthusiastic supporters will place their hopes on the new coach. If we replace the sponsor with shareholders of a listed company, it is natural for shareholders (sponsors) to seek to replace the CEO (equivalent to the coach in the soccer team) of a company with poor strategy and performance. Under the corporate governance system, where shareholders appoint a board of directors based on the agency theory to nominate, appoint, and dismiss the CEO, it is natural for shareholders to propose a board composition that enables them to achieve appropriate CEO succession. In professional soccer, where there are virtually no cases of dominant sponsors (shareholders) such as founders or parent companies also serving as coaches (top management), the corporate governance system seems to function much more simply than in the corporate world. In a situation where a team keeps losing games and is relegated from the first division to the second or third division, it clearly becomes increasingly difficult for a coach to continue being loved by all stakeholders and continue in his/her role. If the readers (the listed companies they belong to) were the sponsors, they would not tolerate such a coach.Column 8. Stable shareholders and the market for corporate control

We have already mentioned that traditional “stable shareholders” (Note 10) are disappearing as an obstacle to the establishment of a market for corporate control. However, the utility of “anchor shareholders” (Note 11) - long-term stable shareholders capable of consistently supporting corporate strategy from a long-term perspective - has been advocated by leading experts (Note 12) in corporate governance research (Note 13). I believe there is room to explore the utility of anchor shareholders in enhancing corporate competitiveness after Japan has achieved a certain degree of structural reform through policy measures. This is merely a personal observation, but for the time being, the Bank of Japan (BOJ) and Government Pension Investment Fund (GPIF), which are universal owners of Japanese companies through ETFs and passive investments, could serve as pseudo-anchor shareholders. As asset owners that are not currently taking proactive shareholder actions, these two entities could play a more proactive role in supporting the sustainable value creation of Japanese companies. I wonder if any specific scheme could be considered in conjunction with the exit strategy for the BOJ's ETF investments.

(Note 10) This mainly refers to cross-shareholding practices.

(Note 11) “Anchor” refers to an anchor = ‘kusari’ in Japanese.

(Note 12) Based on research by Colin Mayer (Emeritus Professor, Saïd Business School, University of Oxford) and others.

(Note 13) See Research Institute of Capital Formation, Development Bank of Japan.

Governance Reforms from Comparative Perspectives: The Capital Market, Ownership and Control. 1 Jul. 2020.